Mobile Banking: UX Research to Redesign 手机银行数字化转型

About

A regional commercial bank in Southeast China was advancing its digital transformation. They commissioned this project to rebuild the mobile banking application.

The engagement covered the full cycle from user research to design execution — and was received with strong recognition from both client and users, leading directly to a follow-on WeChat mini-program redesign.

Challenge

As a regional rural commercial bank, the client served a user base with needs that differed significantly from mainstream fintech. The challenge was improving retention against platforms that had already set high product standards.

Another challenge was organizational. The bank had a layered stakeholder structure where decisions rarely moved in a single direction.

Solution

We understood the users deeply, then anchored every recommendation in user evidence — behavioral observations, task failure rates, and verbatim quotes — and carried that research through to design, not stopping at a report. This gave us a consistent basis to navigate organizational disagreement, and ensured design decisions were traceable back to what users actually needed.

Process

User Insights

Three segments emerged, defined not by age alone but by their relationship with the app. The majority of users came from lower-tier cities and rural areas — with deeply local financial habits, lower average digital literacy, and a stronger reliance on in-person service than typical fintech users.

Across all segments, users positioned the app as a financial tool. Simplicity, reliability, and security mattered far more than feature breadth.

UX Pain Points

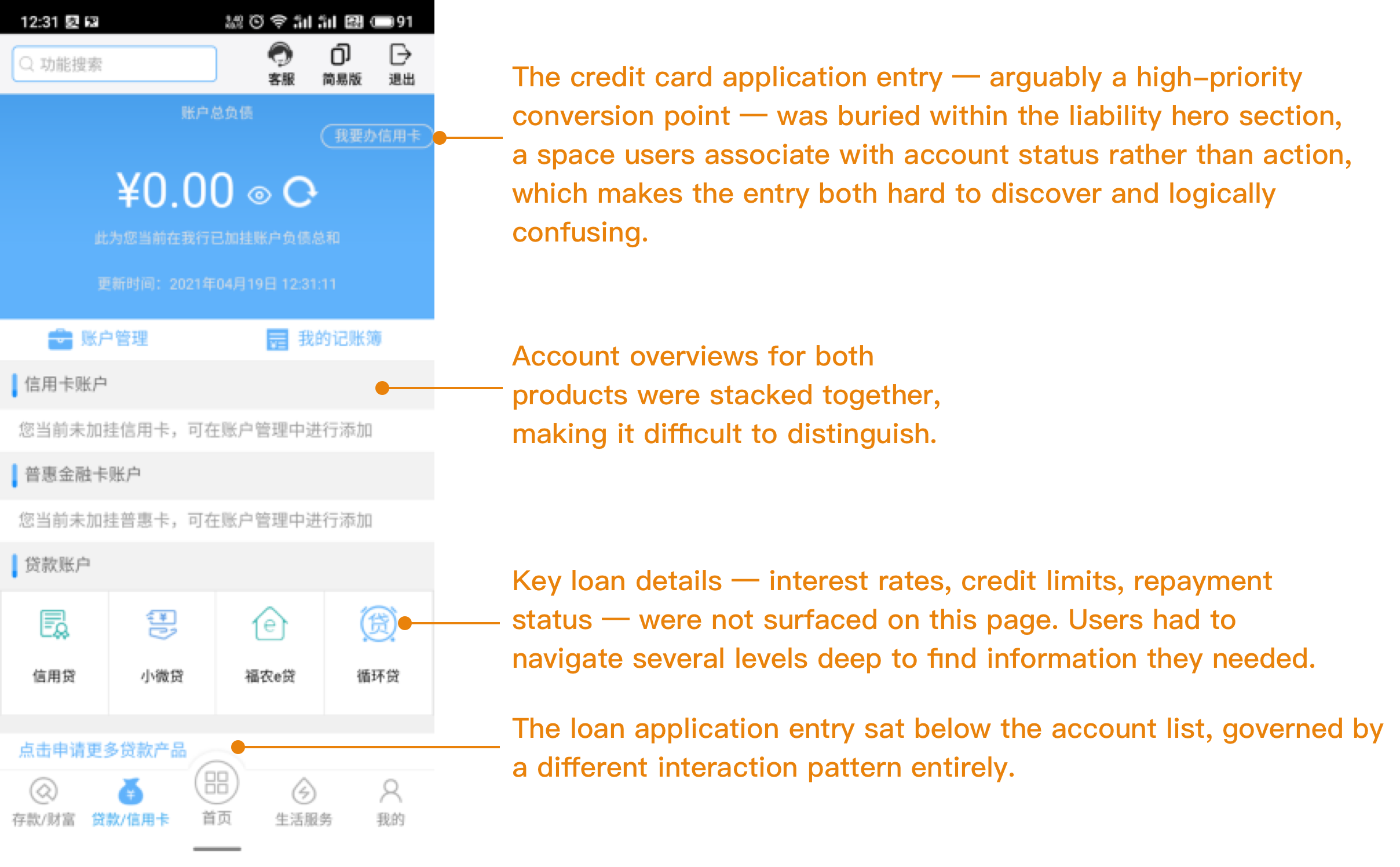

# Cluttered Structure, Hidden Information

The Credit & Loan homepage mixed two distinct services with no clear separation.

The result was a module that felt neither like a credit card page nor a loan page — leaving users unable to locate key information or find the actions they needed.

”I’d prefer the credit card and loan sections to be separate — having them together makes it harder to navigate."

"I do check the card application page, but the apply button text is so small I’d easily miss it."

"The loan page isn’t clear about what it’s for. It’s not intuitive, and the information isn’t presented clearly enough.”

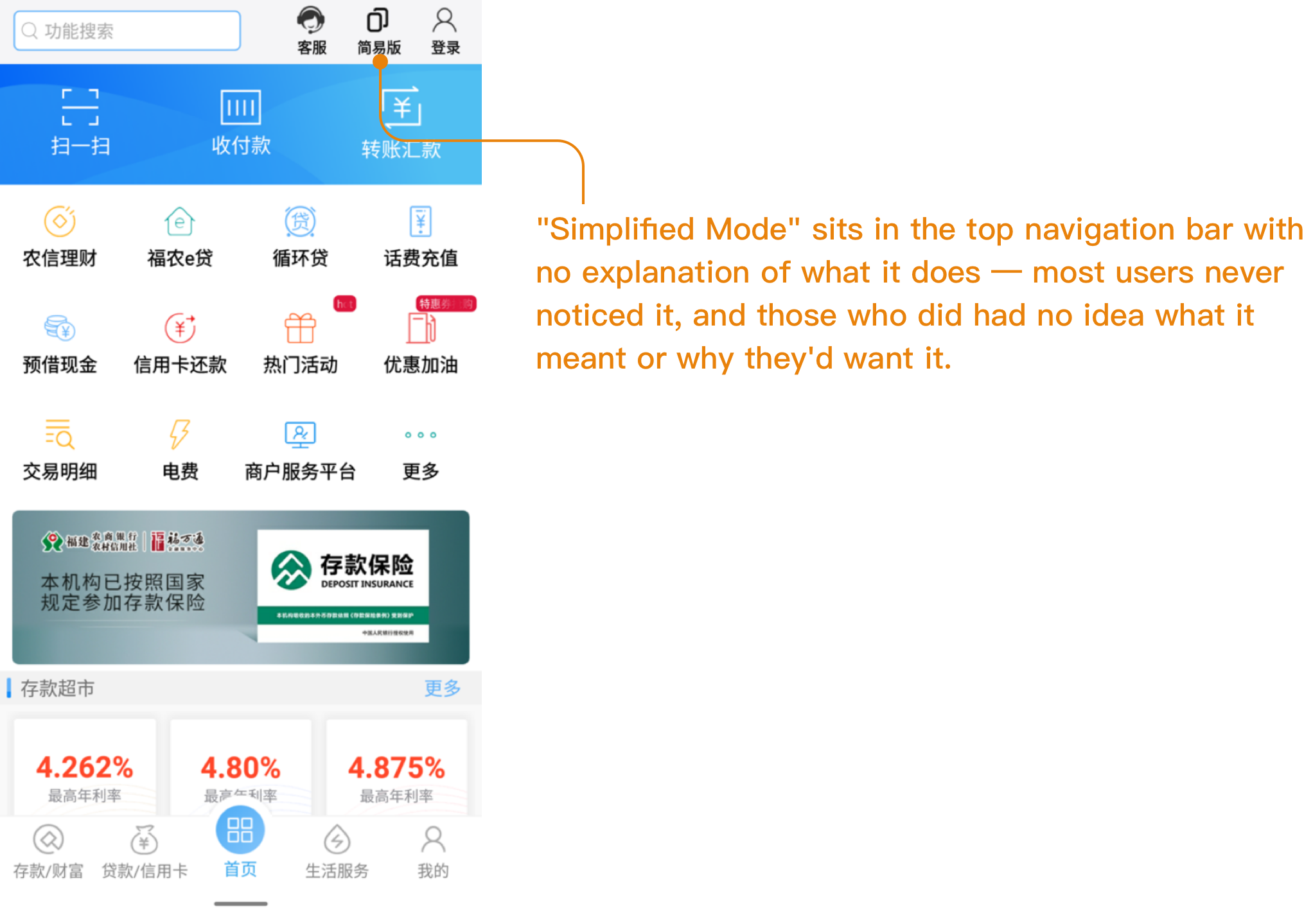

# No Onboarding, No Guidance

The app offered no onboarding flow and no guidance for new users. Without a safety net for mistakes, users avoided exploring unfamiliar features — the care mode entry point was just one example of a useful function that went undiscovered.

”I never noticed the simplified version — the entry point wasn’t obvious at all."

"Banking apps deal with money — I’m afraid to tap things I don’t understand.”

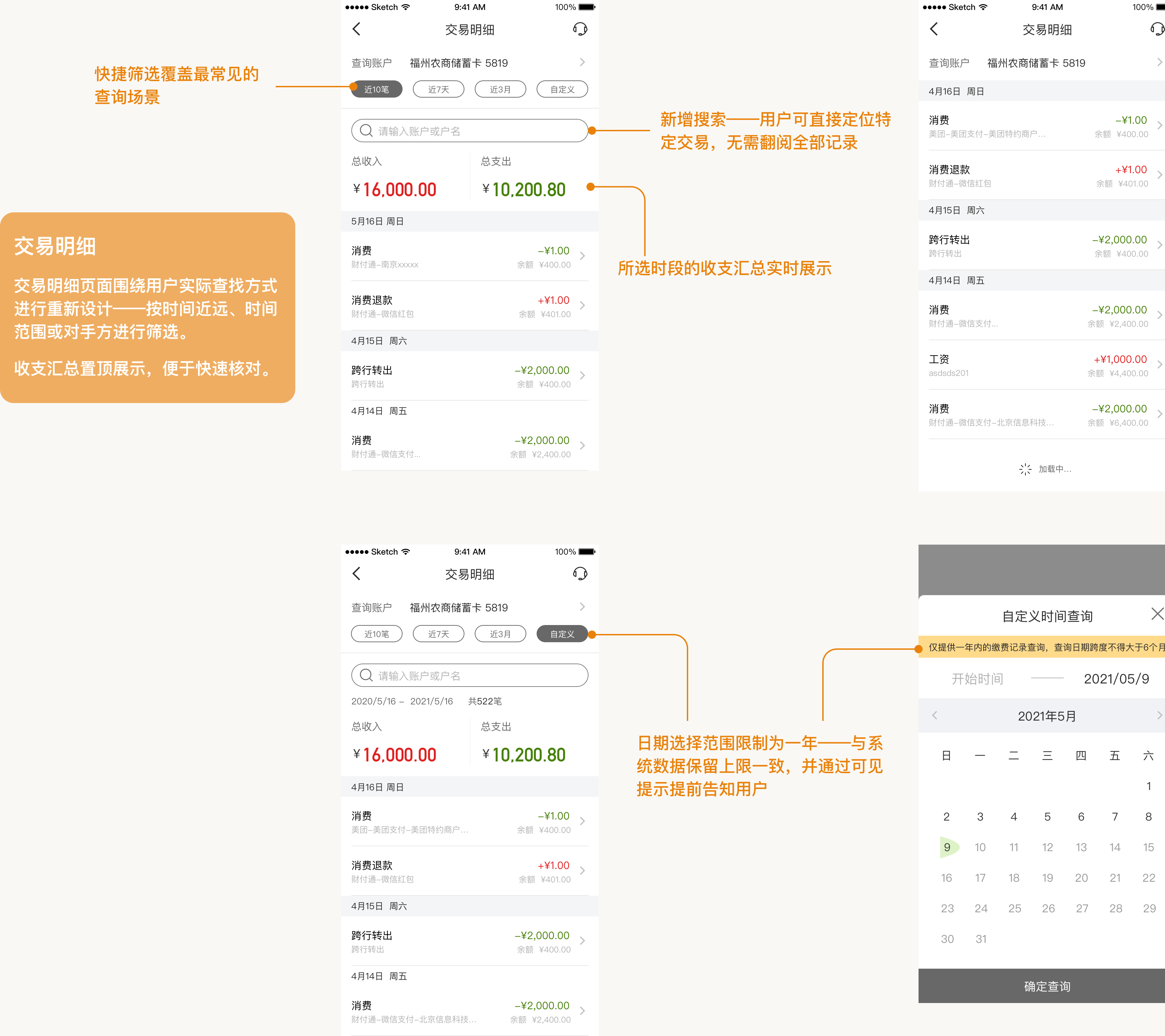

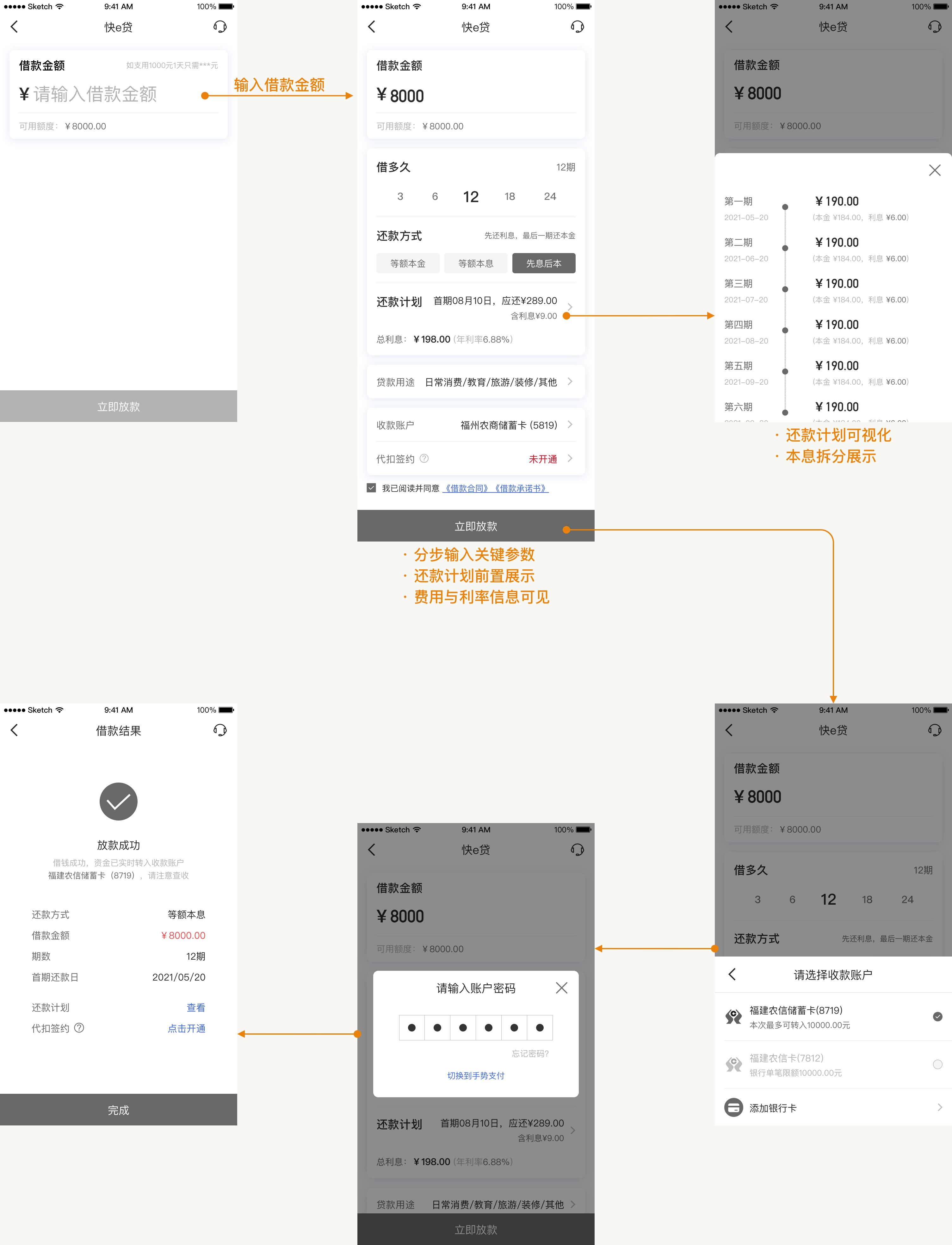

# Complex Flows

Across multiple core flows, users encountered too many steps, unclear progress indicators, and ambiguous outcomes — leaving them unsure whether they had completed a task correctly, or whether anything had happened at all.

”The whole process is such a hassle — I’d rather just go to the branch in person."

"I couldn’t tell how many steps there were in total, or what some of them were even asking me to do.”

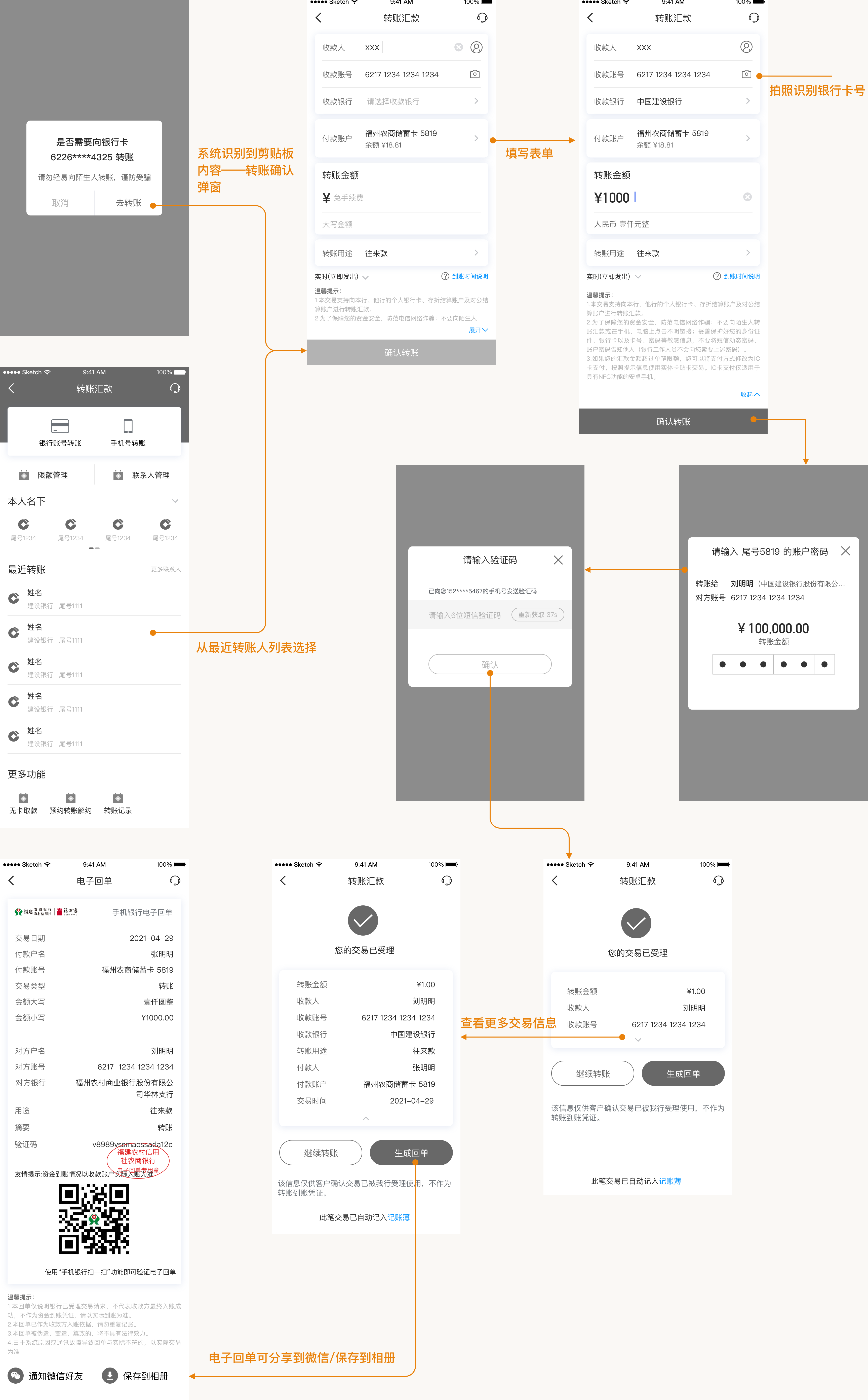

# Friction-Heavy Input

Users repeatedly requested small but high-impact shortcuts — particularly around transfer and life services — that would eliminate manual input and reduce friction in everyday tasks.

”Entering the recipient’s card number is so tedious — it’d be great if I could just take a photo of the card."

"When I copy an account number and switch to the app, I wish it would ask if I want to transfer to that account."

"For mobile top-ups, it should just detect my phone number automatically.”

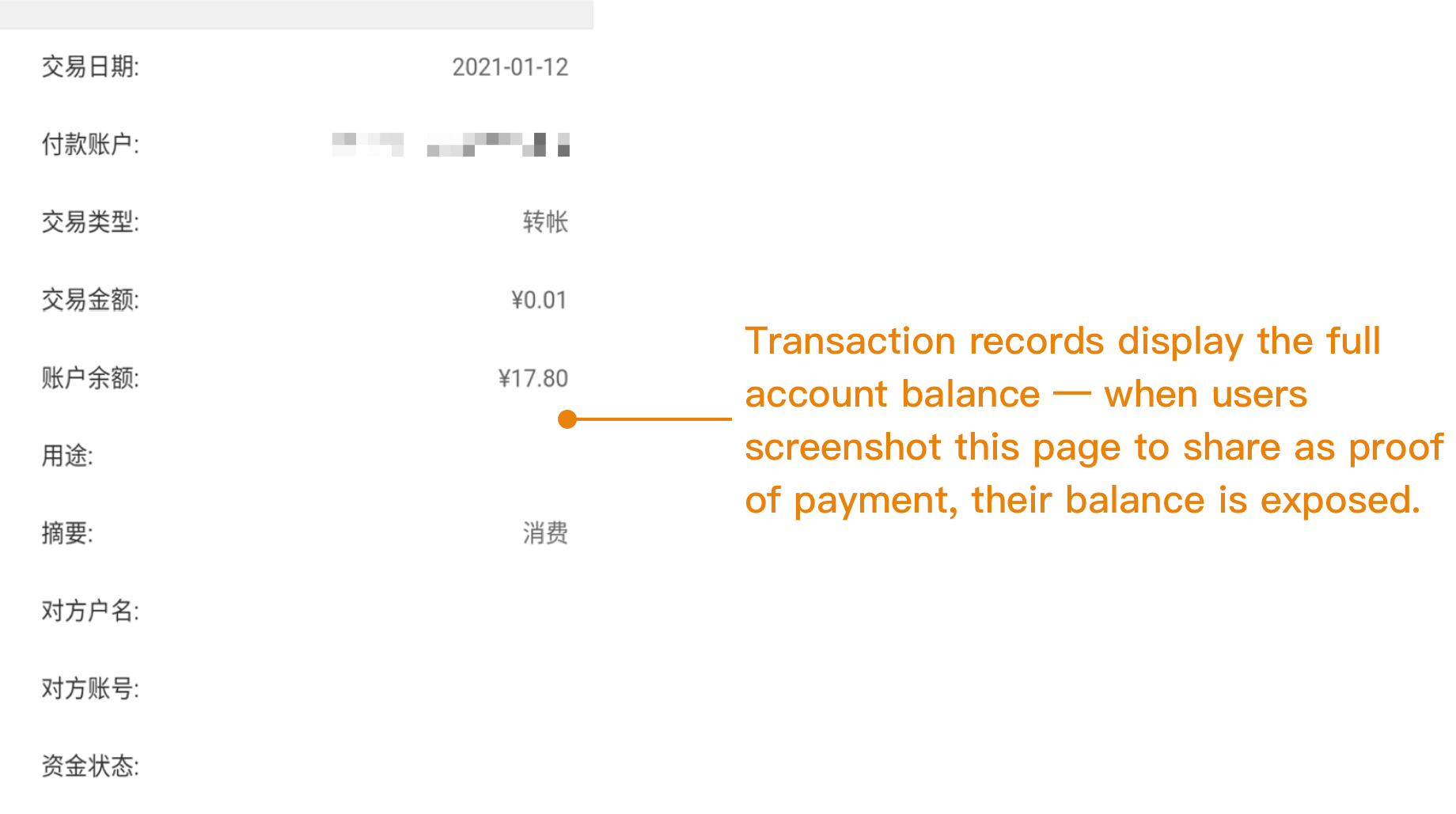

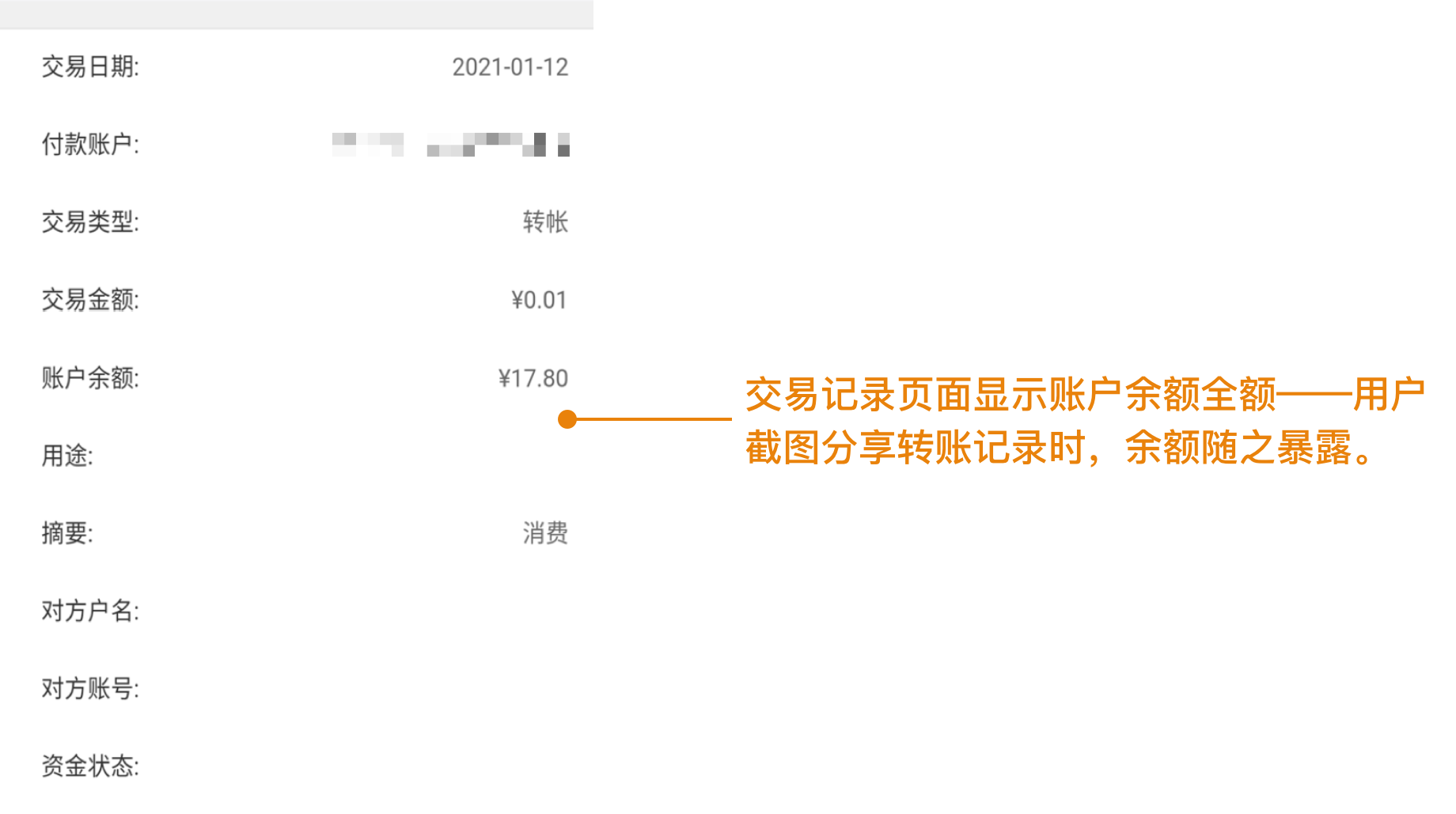

# Unguarded Privacy

The app exposed account balance in every transaction screenshot, and offered no in-app channel for users to communicate securely with their relationship manager.

”When I share a screenshot, my balance shows — I have to edit it out with a photo app."

"I usually talk to my relationship manager over WeChat — I do worry about whether it’s safe.”

From Research to Screen

The findings translated into redesign decisions across three levels. The information architecture was rebuilt to clarify structure and reduce cognitive load. Key modules were restructured to separate what had been conflated. Core flows were streamlined to reduce steps and surface the right information at the right moment. Besides, new capabilities such as privacy controls were added where research identified clear gaps.

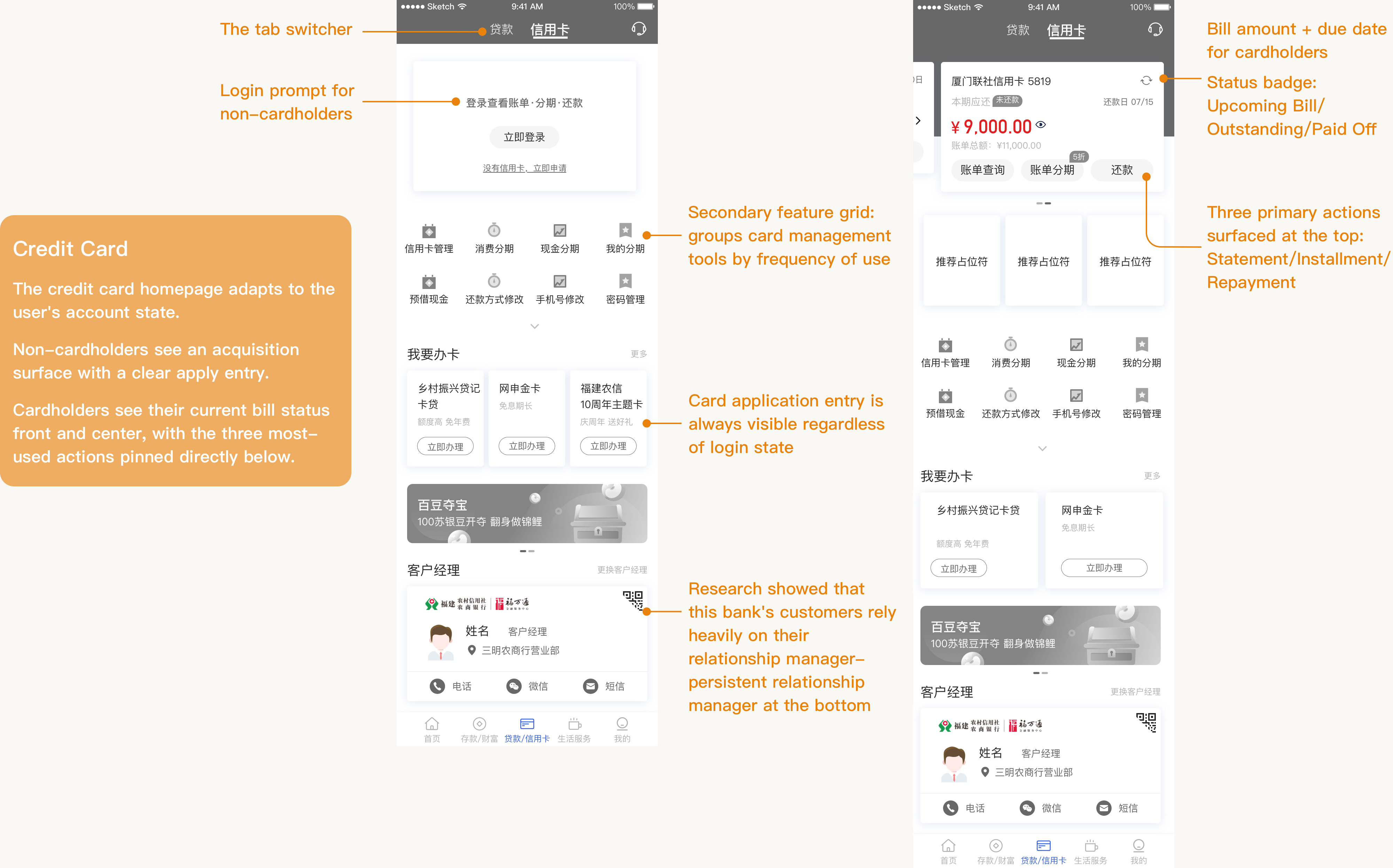

The solution: keep them under the same navigation tab, but introduce a tab switcher at the top so each gets its own dedicated homepage, structured around its own primary tasks.

Follow-On: WeChat Mini-Program

Following the main engagement, the team was commissioned to redesign the WeChat mini-program. Built directly on the UI standards established during the banking app project, interaction prototypes were delivered at high-fidelity — a selection is shown here.

Reflection

Being involved across both research and prototyping made the gap between insight and implementation very visible. Research surfaces what’s broken; design has to decide what’s actually fixable within constraints. That selection process is where most of the real judgment happens — and it’s harder to explain than the research itself.

Anchoring every recommendation in user evidence turned out to serve a different purpose than I expected. It wasn’t just about convincing stakeholders — it was about maintaining internal consistency across a project that ran for months, with multiple rounds of review and revision.

If I were to do this again, I’d push for usability testing on the interaction prototypes earlier. We validated the research direction at scale, but the design decisions themselves were mostly evaluated through heuristic evaluation and client review rather than testing with actual users.

概述

某地区性农村商业银行正推进数字化转型,委托本项目对手机银行进行全面改版。

本次合作覆盖从用户研究到设计落地的完整链路——交付成果获得客户与用户的高度认可,并直接促成了后续微信小程序端的改版项目。

挑战

作为区域性农村商业银行,客户所服务的用户群体与主流金融科技平台有显著差异,如何在用户标准已被头部 app 拉高的市场环境下提升产品留存率,是核心挑战。

另一个挑战来自内部。银行的利益相关方结构较为复杂,各方在方向上并非总能达成共识。

解决方案

深入了解用户,将每一条建议都扎根于用户证据——行为观察、任务失败率、访谈原话——并将研究贯穿整个设计流程,而非止步于报告。这为我们在组织分歧中保持一致立场提供了依据,也确保每一项设计决策都能追溯至用户的真实需求。

项目过程

用户洞察

三类用户群体呈现出明显分层——主要来自下沉市场与县域地区,深度嵌入本地金融习惯,数字化能力相对偏低,对线下服务的依赖程度高于典型金融科技用户。划分依据不只是年龄,更是他们与手机银行的关系模式:

三类群体共同指向一个核心洞察:用户将手机银行定位为专业金融工具,简洁、安全感、可靠性的优先级远高于功能广度。

产品痛点

# 架构混乱,信息隐埋

贷款/信用卡首页将两类截然不同的服务混合呈现,缺乏清晰分层。

结果是这个模块既不像信用卡页面,也不像贷款页面,用户既找不到关键信息,也触达不到需要的操作入口。

“信用卡和贷款放一起太混乱了,我不知道去哪里找我要的东西。"

"贷款页面不知道是干嘛的,逻辑不清楚,信息也没有摆清楚。”

# 缺乏引导

应用没有新手引导流程,也没有任何功能说明。没有容错保护,用户不敢探索——关怀版入口只是众多未被发现的功能之一。

“简易版没注意,切换不明显。"

"银行APP涉及到安全问题,不敢乱点。”

# 流程繁琐

多个核心流程步骤冗长、进度不透明、操作结果模糊——用户不确定自己有没有完成,也不知道下一步是什么。

“整个流程很麻烦,还不如直接去线下申请了。”

# 输入摩擦过高

用户在转账和生活服务场景中反复提出便捷功能需求——减少手动输入、消除重复操作。

“对方卡号输入太麻烦了,能不能拍照识别?"

"希望话费充值自动识别手机号。”

# 隐私保护缺失

应用没有提供任何分享隐私控制——截图时账户余额始终可见。同时用户只能通过微信或电话与客户经理沟通,敏感金融对话游离于任何安全渠道之外。

“截图给人家看的时候余额会展现出来,会用P图软件P掉。"

"经常用微信跟客户经理沟通,担心安全泄漏。“

从研究到落地

研究结论转化为三个层面的设计决策。信息架构重建以理清结构、降低认知负荷;关键模块重组以区分原本混淆的功能;核心流程简化以减少步骤并在恰当时机呈现关键信息。此外,基于用户反馈新增了多项便捷功能及隐私保护机制。

后续:微信小程序

主项目完成后,团队受委托对微信小程序进行改版。设计基于手机银行已建立的 UI 规范,因此交互原型直接以高保真形式交付——此处展示其中一部分。

复盘

研究与原型设计的全程参与,让我清楚地看到了洞察与落地之间的距离。研究揭示了什么是问题;设计则必须在现实约束中决定什么是可以解决的。这个取舍过程才是真正考验判断力的地方——而且往往比研究本身更难解释清楚。

将每一条建议都锚定于用户证据,最终发挥了我没有预料到的作用。它不只是用来说服客户,更是在一个历时数月、经历多轮评审的项目中维持内部一致性的关键。

如果重来,我会更早推动对交互原型做可用性测试。研究方向通过大规模问卷得到了验证,但设计决策本身基本依赖启发式评估和客户评审,而非真实用户测试。